Comprehensive Tutorial: Stochastic Reserving Models

R. Mark Sharp

2026-01-24

comprehensive_tutorial.RmdIntroduction

This tutorial demonstrates all five stochastic reserving models

implemented in the stochasticreserver package: 1.

Chain Ladder - Standard development factor approach 2.

Cape Cod (Bornhuetter-Ferguson variant) -

Exposure-based method 3. Berquist-Sherman - Incremental

severity method with trend 4. Hoerl Curve - Smooth

curve with shared operational time parameters 5. Wright

- Generalized Hoerl with individual accident year levels

These methods are based on Roger Hayne’s paper “A Flexible Framework for Stochastic Reserving Models” published in Variance journal (PDF). The key insight is that all five methods can be unified under a common maximum likelihood estimation framework, enabling consistent uncertainty quantification.

Theoretical Framework

Uncertainty in Loss Reserving

Loss reserve estimates face three distinct sources of uncertainty:

Process Uncertainty - Inherent stochastic fluctuation in outcomes even when parameters are known exactly. This represents the irreducible randomness in insurance claim development.

Parameter Uncertainty - Error from estimating unknown parameters. Even with the correct model structure, finite data leads to estimation error.

Model Uncertainty - Risk that the assumed model structure doesn’t match actual data-generating processes. Different reserving methods may yield different estimates, revealing where assumptions require investigation.

This package addresses process and parameter uncertainty through maximum likelihood estimation (MLE). Model uncertainty is addressed by enabling comparison across multiple methods.

Maximum Likelihood Estimation

MLEs have desirable asymptotic properties (as sample size increases):

- Consistency: Estimates converge to true parameter values

- Efficiency: Variance achieves the theoretical lower bound (Cramér-Rao)

- Asymptotic Normality: Distribution approaches Gaussian with mean and covariance equal to the inverse Fisher information matrix

The Fisher Information Matrix is:

This enables uncertainty quantification through the variance-covariance matrix .

Stochastic Model for Incremental Averages

All models share a common likelihood structure. For incremental averages (where = accident year, = development lag), we assume:

The expected value is model-specific (Chain Ladder, Cape Cod, etc.), while the variance structure is shared:

where:

- is a proportionality constant

- where is the exposure count for accident year

- is a power parameter controlling heteroscedasticity

Negative Log-Likelihood Function

For a single observation, the negative log-likelihood is:

The total objective function sums over all available cells in the triangle.

The Five Model Forms

Each model specifies a different expected value function : | Model | Expected Value Form | Parameters | |——-|———————|————| | Chain Ladder | | Development proportions (sum to 1) | | Cape Cod | | Level + row/column factors | | Berquist-Sherman | | Year levels + trend | | Hoerl Curve | | Curve params + row trend | | Wright | | Individual levels + curve |

where represents operational time (development lag) and represents the ultimate for accident year .

Gradient and Hessian

Efficient optimization requires analytical gradients and Hessians. For parameter vector :

Gradient with respect to model parameters:

Gradient with respect to variance parameters:

The Hessian matrix enables Newton-type optimization and provides the information matrix for uncertainty quantification.

Data

Package Data: Hayne’s Example Triangle

The package includes data from the reference paper - a 10x10

development triangle of cumulative averages (B0) and

exposure counts (dnom).

# Load the cumulative average triangle

B0 <- stochasticreserver::B0

dnom <- stochasticreserver::dnom

size <- nrow(B0)

# Display the triangle

cat("Cumulative Average Triangle (B0):\n")## Cumulative Average Triangle (B0):## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9]

## [1,] 670.26 1480.25 1938.54 2466.25 2837.85 3003.52 3055.39 3132.94 3141.19

## [2,] 767.99 1592.50 2463.79 3019.72 3374.73 3553.61 3602.28 3627.28 3645.57

## [3,] 740.58 1615.80 2345.85 2910.53 3201.52 3417.71 3506.59 3529.00 NA

## [4,] 862.12 1754.90 2534.78 3270.85 3739.89 4003.00 4125.31 NA NA

## [5,] 840.94 1859.03 2804.55 3445.35 3950.47 4185.95 NA NA NA

## [6,] 848.00 2052.92 3076.14 3861.03 4351.58 NA NA NA NA

## [7,] 901.77 1927.89 3003.59 3881.42 NA NA NA NA NA

## [8,] 935.20 2103.98 3181.75 NA NA NA NA NA NA

## [9,] 759.32 1584.91 NA NA NA NA NA NA NA

## [10,] 723.30 NA NA NA NA NA NA NA NA

## [,10]

## [1,] 3159.73

## [2,] NA

## [3,] NA

## [4,] NA

## [5,] NA

## [6,] NA

## [7,] NA

## [8,] NA

## [9,] NA

## [10,] NA

cat("\nExposure Counts (dnom):\n")##

## Exposure Counts (dnom):## [1] 39161 38672 41801 42263 41481 40214 43599 42118 43479 49492Data Preparation

We need to prepare several derived quantities for the models:

# Calculate incremental average matrix (A0)

A0 <- cbind(B0[, 1], B0[, 2:size] - B0[, 1:(size - 1)])

# Generate log exposure matrix for variance structure

logd <- log(matrix(dnom, size, size))

# Create row and column index matrices

rowNum <- row(A0)

colNum <- col(A0)

# Create masks for data availability

# upper_triangle_mask: TRUE for cells with available data

upper_triangle_mask <- (size - rowNum) >= colNum - 1

# msn: mask for next forecast diagonal (one-period ahead)

msn <- (size - rowNum) == colNum - 2

# msd: mask for current diagonal (paid to date)

msd <- (size - rowNum) == colNum - 1

# Calculate amount paid to date for each accident year

paid_to_date <- rowSums(B0 * msd, na.rm = TRUE)

cat("Paid to Date by Accident Year:\n")## Paid to Date by Accident Year:## [1] 3159.73 3645.57 3529.00 4125.31 4185.95 4351.58 3881.42 3181.75 1584.91

## [10] 723.30Simulated Data: Auto Liability Example

To demonstrate the models on different data characteristics, we also create a simulated dataset representing a stylized auto liability triangle. This simulated data exhibits: - Moderate development over 10 periods - Slight trend in accident year severity - Realistic exposure variation

Note: This data is simulated. For production use, replace with actual public data such as triangles from regulatory filings or industry studies.

set.seed(42)

# Simulate a second triangle with different characteristics

simulate_triangle <- function(n_years = 10, base_ult = 5000, trend = 0.03,

dev_pattern = NULL) {

if (is.null(dev_pattern)) {

# Typical auto liability development pattern

dev_pattern <- c(0.35, 0.25, 0.15, 0.10, 0.06, 0.04, 0.025, 0.015,

0.008, 0.002)

dev_pattern <- dev_pattern / sum(dev_pattern) # Normalize

}

n_dev <- length(dev_pattern)

# Generate ultimates with trend

ultimates <- base_ult * (1 + trend)^(0:(n_years - 1))

ultimates <- ultimates * exp(rnorm(n_years, 0, 0.05)) # Add noise

# Generate incremental averages

incr_avg <- matrix(NA, n_years, n_dev)

for (i in 1:n_years) {

for (j in 1:n_dev) {

if ((n_years - i) >= (j - 1)) {

mu <- ultimates[i] * dev_pattern[j]

sigma <- mu * 0.1 # 10% coefficient of variation

incr_avg[i, j] <- rnorm(1, mu, sigma)

}

}

}

# Convert to cumulative

cum_avg <- t(apply(incr_avg, 1, cumsum))

# Generate exposures (claim counts)

exposures <- round(runif(n_years, 35000, 50000))

list(

B0 = cum_avg,

A0 = incr_avg,

dnom = exposures,

ultimates = ultimates

)

}

sim_data <- simulate_triangle()

B0_sim <- sim_data$B0

A0_sim <- sim_data$A0

dnom_sim <- sim_data$dnom

cat("Simulated Cumulative Triangle:\n")## Simulated Cumulative Triangle:## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9]

## [1,] 2118.72 3763.52 4455.18 4975.73 5292.73 5520.54 5650.60 5709.59 5741.97

## [2,] 1698.59 2727.28 3465.37 4026.84 4384.17 4575.81 4697.76 4759.62 4801.51

## [3,] 1769.59 3181.52 4048.89 4644.97 4949.33 5176.31 5288.17 5362.84 NA

## [4,] 1805.80 2875.26 3724.21 4299.76 4625.90 4868.57 4999.31 NA NA

## [5,] 1734.85 3232.60 4024.08 4681.25 5010.93 5255.69 NA NA NA

## [6,] 2082.96 3411.40 4412.53 5026.17 5375.21 NA NA NA NA

## [7,] 2315.96 4035.05 5009.57 5460.74 NA NA NA NA NA

## [8,] 2203.14 3677.04 4612.09 NA NA NA NA NA NA

## [9,] 2594.93 4591.72 NA NA NA NA NA NA NA

## [10,] 2110.66 NA NA NA NA NA NA NA NA

## [,10]

## [1,] 5754.1

## [2,] NA

## [3,] NA

## [4,] NA

## [5,] NA

## [6,] NA

## [7,] NA

## [8,] NA

## [9,] NA

## [10,] NAHelper Functions

We define helper functions to streamline the analysis across all models.

#' Fit a stochastic reserving model

#'

#' @param model_name Character: "Chain", "CapeCod", "Berquist", "Hoerl",

#' or "Wright"

#' @param B0 Cumulative average matrix

#' @param A0 Incremental average matrix

#' @param dnom Exposure vector

#' @param paid_to_date Paid amounts to date

#' @param upper_triangle_mask Logical mask for available data

#' @return List with fitted model results

fit_model <- function(model_name, B0, A0, dnom, paid_to_date,

upper_triangle_mask) {

size <- nrow(B0)

logd <- log(matrix(dnom, size, size))

# Select model

model_lst <- switch(model_name,

"Chain" = chain(B0, paid_to_date, upper_triangle_mask),

"CapeCod" = capecod(B0, paid_to_date, upper_triangle_mask),

"Berquist" = berquist(B0, paid_to_date, upper_triangle_mask),

"Hoerl" = hoerl(B0, paid_to_date, upper_triangle_mask),

"Wright" = wright(B0, paid_to_date, upper_triangle_mask)

)

g_obj <- model_lst$g_obj

g_grad <- model_lst$g_grad

g_hess <- model_lst$g_hess

a0 <- model_lst$a0

# Get starting values for kappa and p

E <- g_obj(a0)

yyy <- (A0 - E)^2

yyy <- logd + log(((yyy != 0) * yyy) - (yyy == 0))

sss <- na.omit(data.frame(x = c(log(E^2)), y = c(yyy)))

if (nrow(sss) > 2) {

ttt <- array(coef(lm(sss$y ~ sss$x)))[1:2]

} else {

ttt <- c(10, 1)

}

a0 <- c(a0, ttt)

# Objective functions

l.obj <- function(a, A) {

make_negative_log_likelihood(a, A, dnom, g_obj)

}

l.grad <- function(a, A) {

make_gradient_of_objective(a, A, dnom, g_obj, g_grad)

}

l.hess <- function(a, A) {

make_log_hessian(a, A, dnom, g_obj, g_grad, g_hess)

}

# Minimize

max_ctrl <- list(iter.max = 10000, eval.max = 10000)

scale_vec <- abs(1 / (2 * ((a0 * (a0 != 0)) + (1 * (a0 == 0)))))

mle <- tryCatch(

nlminb(a0, l.obj, gradient = l.grad, hessian = l.hess,

scale = scale_vec, A = A0, control = max_ctrl),

error = function(e) {

# Fallback without hessian

nlminb(a0, l.obj, gradient = l.grad,

scale = scale_vec, A = A0, control = max_ctrl)

}

)

# Extract results

npar <- length(mle$par) - 2

p <- mle$par[npar + 2]

mean_fitted <- g_obj(mle$par[1:npar])

var_fitted <- exp(-outer(logd[, 1], rep(mle$par[npar + 1], size), "-")) *

(mean_fitted^2)^p

stres <- (A0 - mean_fitted) / sqrt(var_fitted)

# Information matrix and variance-covariance

hess_final <- l.hess(mle$par, A0)

inf_mat <- tryCatch(

solve(hess_final),

error = function(e) NULL

)

list(

model_name = model_name,

mle = mle,

npar = npar,

mean = mean_fitted,

var = var_fitted,

stres = stres,

g_obj = g_obj,

vcov = inf_mat,

logd = logd,

convergence = mle$convergence

)

}

#' Calculate forecast reserves

#'

#' @param fit Fitted model object

#' @param dnom Exposure vector

#' @param upper_triangle_mask Mask for available data

#' @return Data frame with reserve estimates

calculate_reserves <- function(fit, dnom, upper_triangle_mask) {

size <- nrow(fit$mean)

# Forecast for lower triangle (future payments)

forecast_mask <- !upper_triangle_mask

forecast_mean <- fit$mean * forecast_mask

forecast_var <- fit$var * forecast_mask

# Total reserve by accident year

reserve_mean <- rowSums(dnom * forecast_mean, na.rm = TRUE)

reserve_sd <- sqrt(rowSums(dnom^2 * forecast_var, na.rm = TRUE))

# Aggregate

total_mean <- sum(reserve_mean)

total_sd <- sqrt(sum(dnom^2 * forecast_var, na.rm = TRUE))

data.frame(

accident_year = c(1:size, "Total"),

reserve_mean = c(reserve_mean, total_mean),

reserve_sd = c(reserve_sd, total_sd),

cv = c(reserve_sd / pmax(reserve_mean, 1), total_sd / total_mean)

)

}

#' Run Monte Carlo simulation

#'

#' @param fit Fitted model object

#' @param dnom Exposure vector

#' @param upper_triangle_mask Mask for available data

#' @param nsim Number of simulations

#' @return Matrix of simulated reserves

run_simulation <- function(fit, dnom, upper_triangle_mask, nsim = 5000) {

if (is.null(fit$vcov)) return(NULL)

size <- nrow(fit$mean)

npar <- fit$npar

# Masks for simulation

smsk <- aperm(array(c(upper_triangle_mask), c(size, size, nsim)),

c(3, 1, 2))

# Sample parameters

spar <- tryCatch(

rmvnorm(nsim, fit$mle$par, fit$vcov),

error = function(e) NULL

)

if (is.null(spar)) return(NULL)

# Simulated means

esim <- fit$g_obj(spar)

# Simulated variances

ksim <- exp(aperm(outer(array(spar[, npar + 1], c(nsim, size)),

log(dnom), "-"), c(1, 3, 2)))

psim <- array(spar[, npar + 2], c(nsim, size, size))

vsim <- ksim * (esim^2)^psim

# Simulate future averages

sim_avg <- array(rnorm(nsim * size * size, c(esim), sqrt(c(vsim))),

c(nsim, size, size))

# Calculate reserves

sdnm <- t(matrix(dnom, size, nsim))

reserves <- sdnm * rowSums(sim_avg * !smsk, dims = 2)

cbind(reserves, Total = rowSums(reserves))

}Model Fitting: All Five Methods

Now we fit all five models to the Hayne example data.

model_names <- c("Chain", "CapeCod", "Berquist", "Hoerl", "Wright")

results <- list()

for (model_name in model_names) {

cat("Fitting", model_name, "model...\n")

results[[model_name]] <- fit_model(

model_name, B0, A0, dnom, paid_to_date, upper_triangle_mask

)

cat(" Convergence:", results[[model_name]]$convergence,

" Parameters:", results[[model_name]]$npar + 2, "\n")

}## Fitting Chain model...## Convergence: 0 Parameters: 11

## Fitting CapeCod model...## Convergence: 0 Parameters: 21

## Fitting Berquist model...

## Convergence: 0 Parameters: 13

## Fitting Hoerl model...

## Convergence: 0 Parameters: 7

## Fitting Wright model...

## Convergence: 0 Parameters: 15Model 1: Chain Ladder

The Chain Ladder model represents the standard actuarial approach where development factors link successive development periods. In this stochastic formulation, the expected emergence is parameterized such that development proportions sum to 1.

Parameters

chain_fit <- results[["Chain"]]

cat("Chain Ladder Model\n")## Chain Ladder Model

cat("==================\n")## ==================

cat("Number of parameters:", chain_fit$npar + 2, "\n")## Number of parameters: 11

cat(" - Model parameters:", chain_fit$npar, "(development proportions)\n")## - Model parameters: 9 (development proportions)

cat(" - Variance parameters: 2 (kappa, p)\n\n")## - Variance parameters: 2 (kappa, p)

# Development pattern implied

npar <- chain_fit$npar

theta <- chain_fit$mle$par[1:npar]

dev_pattern <- c(theta, 1 - sum(theta))

cat("Implied development pattern:\n")## Implied development pattern:## Lag1 Lag2 Lag3 Lag4 Lag5 Lag6 Lag7 Lag8 Lag9 Lag10

## 0.1955 0.2307 0.2077 0.1637 0.1043 0.0555 0.0217 0.0132 0.0030 0.0047##

## Cumulative: 0.1955 0.4262 0.6339 0.7976 0.9019 0.9574 0.9791 0.9922 0.9953 1Fitted Values

cat("\nFitted Mean (expected incremental averages):\n")##

## Fitted Mean (expected incremental averages):## [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10]

## [1,] 617.57 729.07 656.33 517.19 329.57 175.45 68.44 41.59 9.51 15.00

## [2,] 715.93 845.18 760.86 599.57 382.05 203.39 79.34 48.21 11.03 17.39

## [3,] 695.14 820.64 738.77 582.16 370.96 197.49 77.04 46.81 10.71 16.89

## [4,] 823.53 972.20 875.21 689.67 439.47 233.96 91.26 55.46 12.69 20.00

## [5,] 854.54 1008.81 908.16 715.64 456.02 242.77 94.70 57.55 13.16 20.76

## [6,] 943.04 1113.30 1002.22 789.76 503.25 267.91 104.51 63.51 14.53 22.91

## [7,] 951.15 1122.87 1010.84 796.55 507.58 270.22 105.41 64.05 14.65 23.11

## [8,] 981.03 1158.13 1042.59 821.57 523.52 278.70 108.72 66.07 15.11 23.83

## [9,] 726.85 858.06 772.46 608.70 387.88 206.49 80.55 48.95 11.20 17.66

## [10,] 723.30 853.88 768.69 605.74 385.99 205.48 80.16 48.71 11.14 17.57Reserve Estimates

chain_reserves <- calculate_reserves(chain_fit, dnom, upper_triangle_mask)

knitr::kable(chain_reserves, digits = 0,

caption = "Chain Ladder Reserve Estimates")| accident_year | reserve_mean | reserve_sd | cv |

|---|---|---|---|

| 1 | 0 | 0 | 0 |

| 2 | 672557 | 473869 | 1 |

| 3 | 1153495 | 628724 | 1 |

| 4 | 3725552 | 1068158 | 0 |

| 5 | 7722556 | 1489549 | 0 |

| 6 | 19036072 | 2214503 | 0 |

| 7 | 42945172 | 3195515 | 0 |

| 8 | 77393393 | 4157471 | 0 |

| 9 | 92779952 | 4551418 | 0 |

| 10 | 147356872 | 5671774 | 0 |

| Total | 392785621 | 9447957 | 0 |

Model 2: Cape Cod (Bornhuetter-Ferguson)

The Cape Cod model incorporates exposure information through a multiplicative structure with row (accident year) and column (development) factors. This allows for prior information about ultimate severity levels.

Parameters

cc_fit <- results[["CapeCod"]]

cat("Cape Cod Model\n")## Cape Cod Model

cat("==============\n")## ==============

cat("Number of parameters:", cc_fit$npar + 2, "\n")## Number of parameters: 21

cat(" - Model parameters:", cc_fit$npar, "\n")## - Model parameters: 19

cat(" - 1 level parameter\n")## - 1 level parameter

cat(" -", (size - 1), "row factors\n")## - 9 row factors

cat(" -", (size - 1), "column factors\n")## - 9 column factors

cat(" - Variance parameters: 2\n")## - Variance parameters: 2Reserve Estimates

cc_reserves <- calculate_reserves(cc_fit, dnom, upper_triangle_mask)

knitr::kable(cc_reserves, digits = 0,

caption = "Cape Cod Reserve Estimates")| accident_year | reserve_mean | reserve_sd | cv |

|---|---|---|---|

| 1 | 0 | 0 | 0 |

| 2 | 675487 | 478362 | 1 |

| 3 | 1154053 | 633975 | 1 |

| 4 | 3705613 | 1071770 | 0 |

| 5 | 7709391 | 1494876 | 0 |

| 6 | 19040687 | 2219174 | 0 |

| 7 | 42938949 | 3196213 | 0 |

| 8 | 77307054 | 4150959 | 0 |

| 9 | 92581984 | 4542194 | 0 |

| 10 | 147002026 | 5656751 | 0 |

| Total | 392115245 | 9434799 | 0 |

Model 3: Berquist-Sherman

The Berquist-Sherman model is an incremental severity method that explicitly models trend over development periods. This is particularly useful when development patterns are changing over time.

Parameters

berq_fit <- results[["Berquist"]]

cat("Berquist-Sherman Model\n")## Berquist-Sherman Model

cat("======================\n")## ======================

cat("Number of parameters:", berq_fit$npar + 2, "\n")## Number of parameters: 13

cat(" - Model parameters:", berq_fit$npar, "\n")## - Model parameters: 11

cat(" -", size, "accident year averages\n")## - 10 accident year averages

cat(" - 1 trend parameter\n")## - 1 trend parameter

cat(" - Variance parameters: 2\n\n")## - Variance parameters: 2

# Extract trend parameter

trend_param <- berq_fit$mle$par[size + 1]

cat("Estimated trend parameter:", round(trend_param, 4), "\n")## Estimated trend parameter: 0.0452## This implies 4.62 % change per development periodReserve Estimates

berq_reserves <- calculate_reserves(berq_fit, dnom, upper_triangle_mask)

knitr::kable(berq_reserves, digits = 0,

caption = "Berquist-Sherman Reserve Estimates")| accident_year | reserve_mean | reserve_sd | cv |

|---|---|---|---|

| 1 | 0 | 0 | 0 |

| 2 | 643872 | 337239 | 1 |

| 3 | 1258406 | 465360 | 0 |

| 4 | 3553041 | 889597 | 0 |

| 5 | 7338748 | 1384118 | 0 |

| 6 | 17011031 | 2408663 | 0 |

| 7 | 40234557 | 4133010 | 0 |

| 8 | 74139470 | 6077538 | 0 |

| 9 | 126323652 | 8355660 | 0 |

| 10 | 209606332 | 11101836 | 0 |

| Total | 480109108 | 15997662 | 0 |

Model 4: Hoerl Curve

The Hoerl model uses a smooth mathematical curve to describe development rather than discrete factors. The curve includes polynomial and logarithmic terms in operational time, plus a row trend.

Parameters

hoerl_fit <- results[["Hoerl"]]

cat("Hoerl Curve Model\n")## Hoerl Curve Model

cat("=================\n")## =================

cat("Number of parameters:", hoerl_fit$npar + 2, "\n")## Number of parameters: 7

cat(" - Model parameters:", hoerl_fit$npar, "\n")## - Model parameters: 5

cat(" - alpha (intercept)\n")## - alpha (intercept)

cat(" - beta1 (linear in tau)\n")## - beta1 (linear in tau)

cat(" - beta2 (quadratic in tau)\n")## - beta2 (quadratic in tau)

cat(" - beta3 (log tau)\n")## - beta3 (log tau)

cat(" - beta4 (row trend)\n")## - beta4 (row trend)

cat(" - Variance parameters: 2\n\n")## - Variance parameters: 2

hoerl_theta <- hoerl_fit$mle$par[1:5]

names(hoerl_theta) <- c("alpha", "beta1", "beta2", "beta3", "beta4")

print(round(hoerl_theta, 4))## alpha beta1 beta2 beta3 beta4

## 6.4977 0.0034 -0.0652 0.5984 0.0430Reserve Estimates

hoerl_reserves <- calculate_reserves(hoerl_fit, dnom, upper_triangle_mask)

knitr::kable(hoerl_reserves, digits = 0,

caption = "Hoerl Curve Reserve Estimates")| accident_year | reserve_mean | reserve_sd | cv |

|---|---|---|---|

| 1 | 0 | 0 | 0 |

| 2 | 169866 | 296971 | 2 |

| 3 | 810147 | 652176 | 1 |

| 4 | 2690392 | 1195122 | 0 |

| 5 | 7354087 | 1986075 | 0 |

| 6 | 17306357 | 3060366 | 0 |

| 7 | 40013505 | 4670729 | 0 |

| 8 | 72642848 | 6311653 | 0 |

| 9 | 124351004 | 8275308 | 0 |

| 10 | 207051137 | 10691966 | 0 |

| Total | 472389343 | 16115325 | 0 |

Model 5: Wright (Generalized Hoerl)

The Wright model extends the Hoerl curve by allowing individual level parameters for each accident year rather than just a linear trend. This provides more flexibility at the cost of additional parameters.

Parameters

wright_fit <- results[["Wright"]]

cat("Wright Model\n")## Wright Model

cat("============\n")## ============

cat("Number of parameters:", wright_fit$npar + 2, "\n")## Number of parameters: 15

cat(" - Model parameters:", wright_fit$npar, "\n")## - Model parameters: 13

cat(" -", size, "individual year levels (alpha_i)\n")## - 10 individual year levels (alpha_i)

cat(" - 3 operational time parameters (beta1, beta2, beta3)\n")## - 3 operational time parameters (beta1, beta2, beta3)

cat(" - Variance parameters: 2\n\n")## - Variance parameters: 2

wright_theta <- wright_fit$mle$par[1:wright_fit$npar]

cat("Accident year levels:\n")## Accident year levels:## [1] 6.3169 6.4758 6.4403 6.5919 6.6407 6.7428 6.7468 6.7756 6.4808 6.4732

cat("\nOperational time parameters:\n")##

## Operational time parameters:

names(wright_theta[(size + 1):(size + 3)]) <- c("beta1", "beta2", "beta3")

print(round(wright_theta[(size + 1):(size + 3)], 4))## [1] 0.1864 -0.0776 0.2975Reserve Estimates

wright_reserves <- calculate_reserves(wright_fit, dnom, upper_triangle_mask)

knitr::kable(wright_reserves, digits = 0,

caption = "Wright Model Reserve Estimates")| accident_year | reserve_mean | reserve_sd | cv |

|---|---|---|---|

| 1 | 0 | 0 | 0 |

| 2 | 137270 | 432966 | 3 |

| 3 | 646137 | 800325 | 1 |

| 4 | 2533412 | 1306997 | 1 |

| 5 | 7277123 | 1888006 | 0 |

| 6 | 18702982 | 2609470 | 0 |

| 7 | 42231067 | 3524225 | 0 |

| 8 | 75946730 | 4334693 | 0 |

| 9 | 92611271 | 4768645 | 0 |

| 10 | 146554330 | 5807424 | 0 |

| Total | 386640322 | 10029257 | 0 |

Model Comparison

Reserve Estimates Comparison

comparison <- data.frame(

Accident_Year = 1:size,

Chain = chain_reserves$reserve_mean[1:size],

CapeCod = cc_reserves$reserve_mean[1:size],

Berquist = berq_reserves$reserve_mean[1:size],

Hoerl = hoerl_reserves$reserve_mean[1:size],

Wright = wright_reserves$reserve_mean[1:size]

)

# Add totals

comparison <- rbind(

comparison,

data.frame(

Accident_Year = "Total",

Chain = chain_reserves$reserve_mean[size + 1],

CapeCod = cc_reserves$reserve_mean[size + 1],

Berquist = berq_reserves$reserve_mean[size + 1],

Hoerl = hoerl_reserves$reserve_mean[size + 1],

Wright = wright_reserves$reserve_mean[size + 1]

)

)

knitr::kable(comparison, digits = 0,

caption = "Reserve Comparison Across Models")| Accident_Year | Chain | CapeCod | Berquist | Hoerl | Wright |

|---|---|---|---|---|---|

| 1 | 0 | 0 | 0 | 0 | 0 |

| 2 | 672557 | 675487 | 643872 | 169866 | 137270 |

| 3 | 1153495 | 1154053 | 1258406 | 810147 | 646137 |

| 4 | 3725552 | 3705613 | 3553041 | 2690392 | 2533412 |

| 5 | 7722556 | 7709391 | 7338748 | 7354087 | 7277123 |

| 6 | 19036072 | 19040687 | 17011031 | 17306357 | 18702982 |

| 7 | 42945172 | 42938949 | 40234557 | 40013505 | 42231067 |

| 8 | 77393393 | 77307054 | 74139470 | 72642848 | 75946730 |

| 9 | 92779952 | 92581984 | 126323652 | 124351004 | 92611271 |

| 10 | 147356872 | 147002026 | 209606332 | 207051137 | 146554330 |

| Total | 392785621 | 392115245 | 480109108 | 472389343 | 386640322 |

Parameter Count Comparison

param_df <- data.frame(

Model = model_names,

Model_Params = sapply(results, function(x) x$npar),

Variance_Params = 2,

Total_Params = sapply(results, function(x) x$npar + 2),

Convergence = sapply(results, function(x) x$convergence)

)

knitr::kable(param_df, caption = "Parameter Count by Model")| Model | Model_Params | Variance_Params | Total_Params | Convergence | |

|---|---|---|---|---|---|

| Chain | Chain | 9 | 2 | 11 | 0 |

| CapeCod | CapeCod | 19 | 2 | 21 | 0 |

| Berquist | Berquist | 11 | 2 | 13 | 0 |

| Hoerl | Hoerl | 5 | 2 | 7 | 0 |

| Wright | Wright | 13 | 2 | 15 | 0 |

Negative Log-Likelihood Comparison

nll_df <- data.frame(

Model = model_names,

NegLogLik = sapply(results, function(x) x$mle$objective),

AIC = sapply(results, function(x) {

2 * (x$npar + 2) + 2 * x$mle$objective

}),

BIC = sapply(results, function(x) {

n_obs <- sum(!is.na(A0) & upper_triangle_mask)

log(n_obs) * (x$npar + 2) + 2 * x$mle$objective

})

)

nll_df <- nll_df[order(nll_df$AIC), ]

knitr::kable(nll_df, digits = 2, row.names = FALSE,

caption = "Model Fit Statistics (sorted by AIC)")| Model | NegLogLik | AIC | BIC |

|---|---|---|---|

| Chain | 288.69 | 599.37 | 621.45 |

| Wright | 291.16 | 612.33 | 642.44 |

| CapeCod | 288.66 | 619.32 | 661.47 |

| Hoerl | 312.86 | 639.71 | 653.76 |

| Berquist | 308.72 | 643.45 | 669.54 |

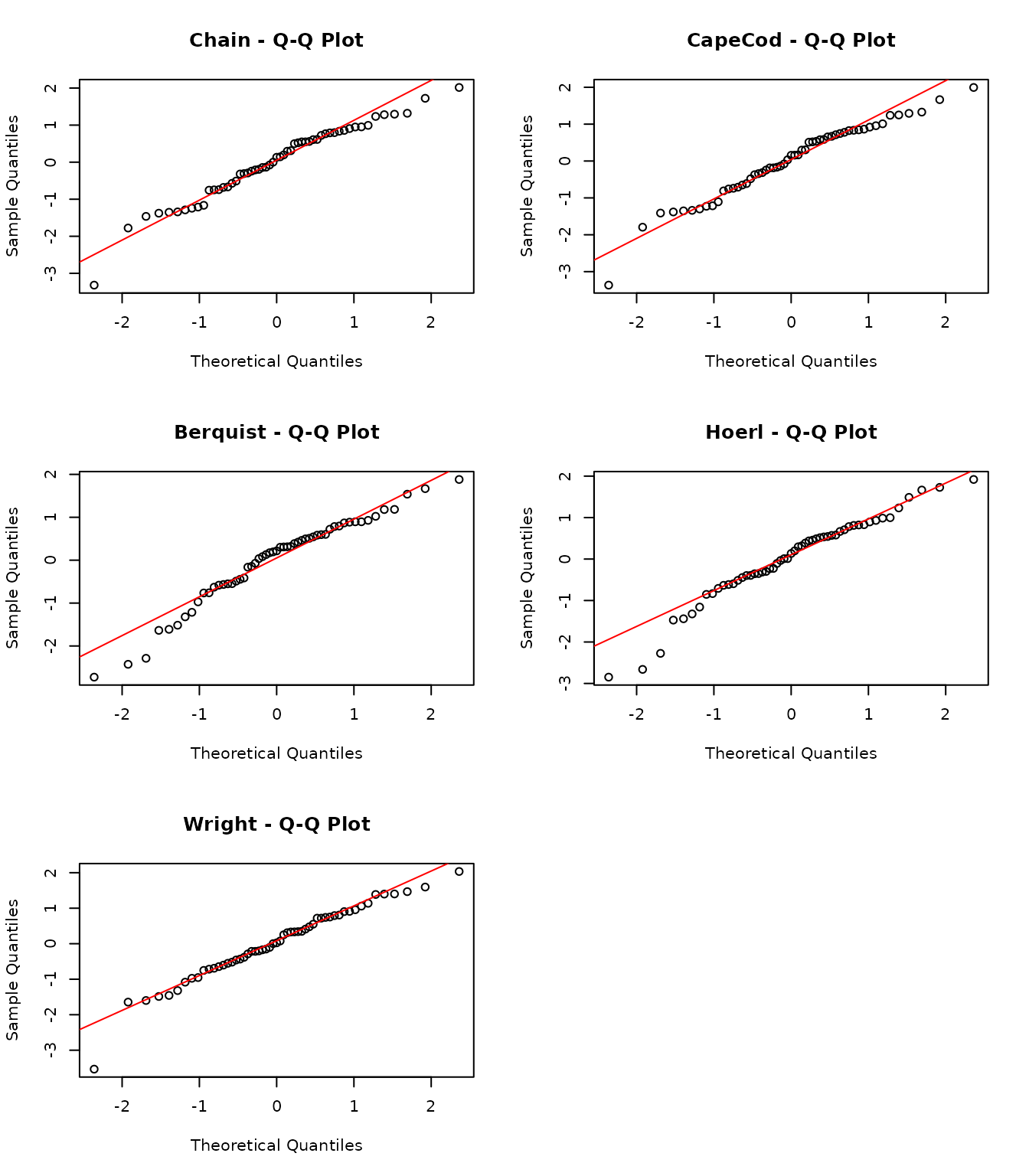

Diagnostic Plots

Residual Analysis

Standardized residuals should be approximately standard normal if the model fits well.

par(mfrow = c(3, 2))

for (model_name in model_names) {

fit <- results[[model_name]]

stres <- fit$stres

# Q-Q plot

qqnorm(c(stres), main = paste(model_name, "- Q-Q Plot"))

qqline(c(stres), col = "red")

}

# Combined residual comparison

par(mfrow = c(1, 1))

Residuals by Calendar Year

par(mfrow = c(2, 3))

for (model_name in model_names) {

fit <- results[[model_name]]

stres <- fit$stres

cy <- rowNum + colNum - 1

plot(c(cy), c(stres),

main = paste(model_name, "- by Calendar Year"),

xlab = "Calendar Year", ylab = "Std Residual",

pch = 16, col = "blue")

abline(h = 0, col = "gray")

# Add mean by CY

cy_means <- tapply(c(stres), c(cy), mean, na.rm = TRUE)

lines(as.numeric(names(cy_means)), cy_means, col = "red", lwd = 2)

}

par(mfrow = c(1, 1))

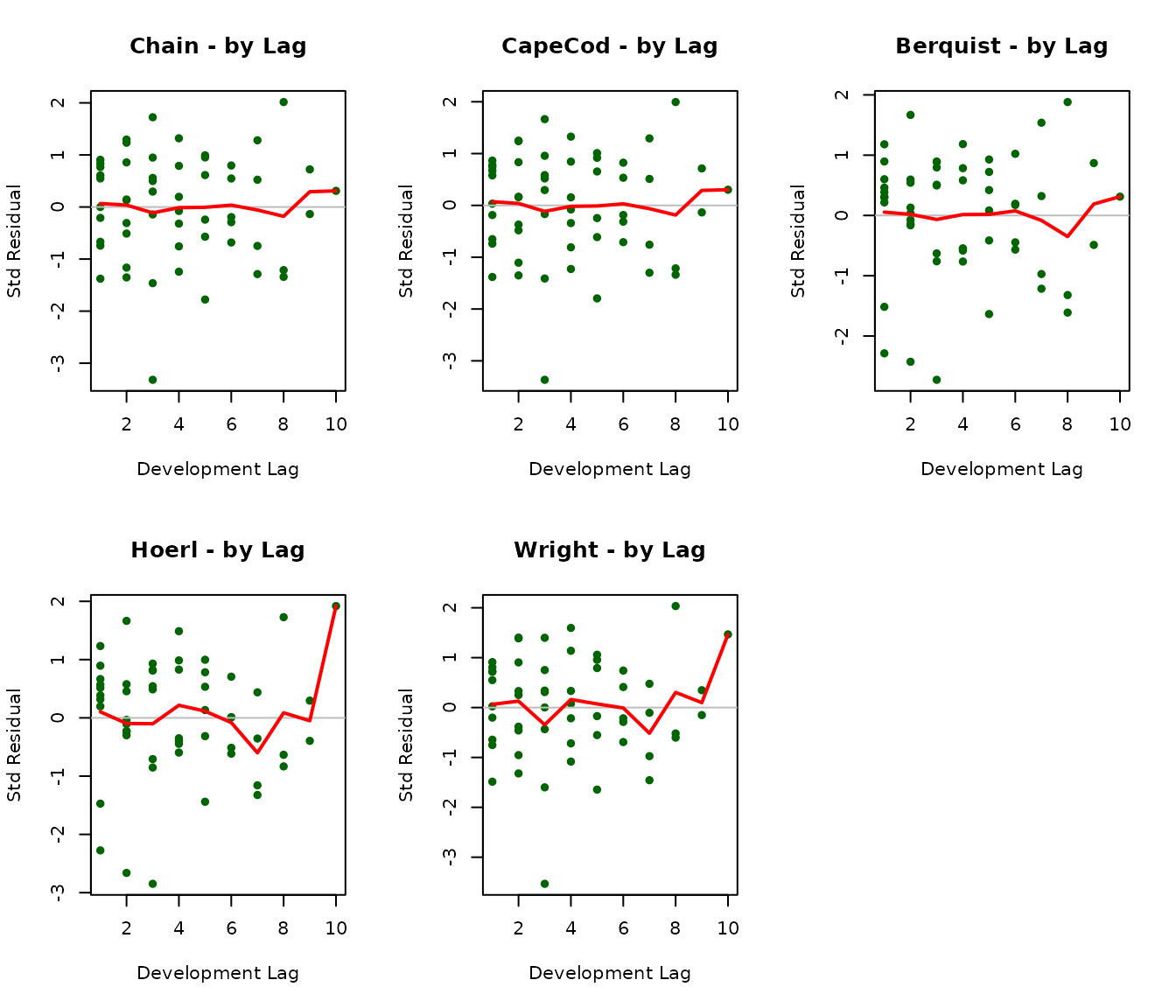

Residuals by Development Lag

par(mfrow = c(2, 3))

for (model_name in model_names) {

fit <- results[[model_name]]

stres <- fit$stres

plot(c(colNum), c(stres),

main = paste(model_name, "- by Lag"),

xlab = "Development Lag", ylab = "Std Residual",

pch = 16, col = "darkgreen")

abline(h = 0, col = "gray")

# Add mean by lag

lag_means <- colMeans(stres, na.rm = TRUE)

lines(1:size, lag_means, col = "red", lwd = 2)

}

par(mfrow = c(1, 1))

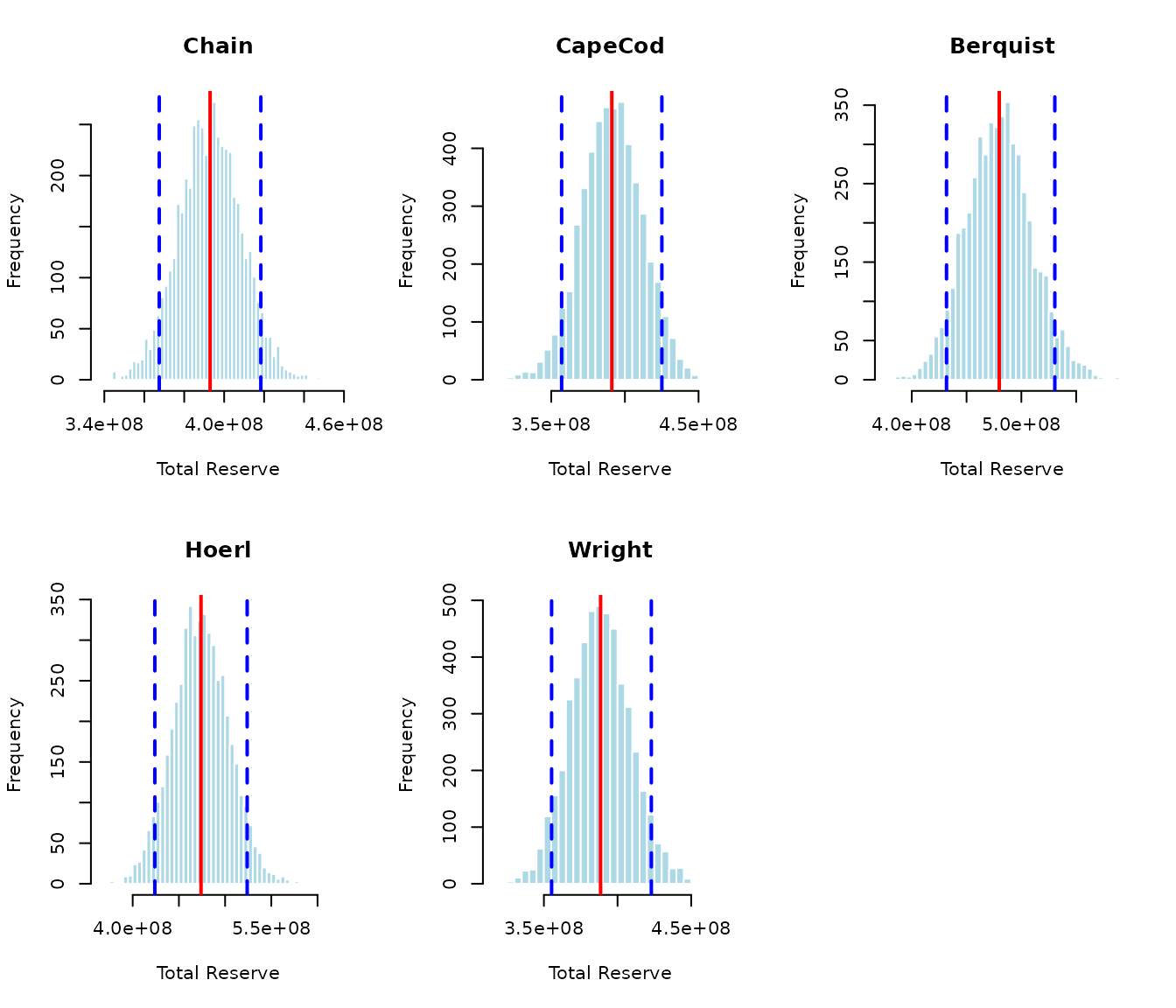

Monte Carlo Simulation

We run simulations to generate full reserve distributions for each model.

set.seed(123)

nsim <- 5000

sim_results <- list()

for (model_name in model_names) {

cat("Running simulation for", model_name, "...\n")

sim_results[[model_name]] <- run_simulation(

results[[model_name]], dnom, upper_triangle_mask, nsim

)

}## Running simulation for Chain ...

## Running simulation for CapeCod ...

## Running simulation for Berquist ...

## Running simulation for Hoerl ...

## Running simulation for Wright ...Distribution of Total Reserves

par(mfrow = c(2, 3))

for (model_name in model_names) {

sim <- sim_results[[model_name]]

if (!is.null(sim)) {

hist(sim[, "Total"], breaks = 50, main = model_name,

xlab = "Total Reserve", col = "lightblue", border = "white")

abline(v = mean(sim[, "Total"]), col = "red", lwd = 2)

abline(v = quantile(sim[, "Total"], c(0.05, 0.95)),

col = "blue", lwd = 2, lty = 2)

}

}

par(mfrow = c(1, 1))

Summary Statistics from Simulation

sim_summary <- data.frame(

Model = character(),

Mean = numeric(),

SD = numeric(),

CV = numeric(),

Q05 = numeric(),

Q50 = numeric(),

Q95 = numeric(),

stringsAsFactors = FALSE

)

for (model_name in model_names) {

sim <- sim_results[[model_name]]

if (!is.null(sim)) {

total <- sim[, "Total"]

sim_summary <- rbind(sim_summary, data.frame(

Model = model_name,

Mean = mean(total),

SD = sd(total),

CV = sd(total) / mean(total),

Q05 = quantile(total, 0.05),

Q50 = quantile(total, 0.50),

Q95 = quantile(total, 0.95)

))

}

}

knitr::kable(sim_summary, digits = 0, row.names = FALSE,

caption = "Simulation Summary: Total Reserves")| Model | Mean | SD | CV | Q05 | Q50 | Q95 |

|---|---|---|---|---|---|---|

| Chain | 392960259 | 15561431 | 0 | 367489169 | 393100561 | 418358515 |

| CapeCod | 391119137 | 20615514 | 0 | 357047772 | 391091786 | 425096127 |

| Berquist | 479838891 | 29994456 | 0 | 431725703 | 479707042 | 530528847 |

| Hoerl | 473934097 | 30221127 | 0 | 423963049 | 473631653 | 523886441 |

| Wright | 388494953 | 20479152 | 0 | 355231550 | 388167747 | 422943246 |

Application to Simulated Data

We now apply all models to the simulated auto liability data to demonstrate robustness across different data characteristics.

# Prepare simulated data

size_sim <- nrow(B0_sim)

logd_sim <- log(matrix(dnom_sim, size_sim, size_sim))

rowNum_sim <- row(A0_sim)

colNum_sim <- col(A0_sim)

upper_triangle_mask_sim <- (size_sim - rowNum_sim) >= colNum_sim - 1

msd_sim <- (size_sim - rowNum_sim) == colNum_sim - 1

paid_to_date_sim <- rowSums(B0_sim * msd_sim, na.rm = TRUE)

results_sim <- list()

for (model_name in model_names) {

cat("Fitting", model_name, "to simulated data...\n")

results_sim[[model_name]] <- fit_model(

model_name, B0_sim, A0_sim, dnom_sim, paid_to_date_sim,

upper_triangle_mask_sim

)

}## Fitting Chain to simulated data...## Fitting CapeCod to simulated data...## Fitting Berquist to simulated data...

## Fitting Hoerl to simulated data...

## Fitting Wright to simulated data...Comparison on Simulated Data

comparison_sim <- data.frame(

Model = model_names,

Reserve = sapply(results_sim, function(x) {

res <- calculate_reserves(x, dnom_sim, upper_triangle_mask_sim)

res$reserve_mean[size_sim + 1]

}),

True_IBNR = sum(sim_data$ultimates * dnom_sim) -

sum(B0_sim * upper_triangle_mask_sim * dnom_sim, na.rm = TRUE)

)

comparison_sim$Error_Pct <- (comparison_sim$Reserve -

comparison_sim$True_IBNR) / comparison_sim$True_IBNR * 100

knitr::kable(comparison_sim, digits = c(0, 0, 0, 1), row.names = FALSE,

caption = "Reserve Estimates vs True IBNR (Simulated Data)")| Model | Reserve | True_IBNR | Error_Pct |

|---|---|---|---|

| Chain | 466237577 | -7763805521 | -106.0 |

| CapeCod | 458610010 | -7763805521 | -105.9 |

| Berquist | 456073545 | -7763805521 | -105.9 |

| Hoerl | 458513352 | -7763805521 | -105.9 |

| Wright | 464082728 | -7763805521 | -106.0 |

Model Selection Guidance

Based on the analysis above, here is guidance for model selection:

When to Use Each Model

Chain Ladder: Best for stable, mature lines with consistent development. Fewest parameters (9) provides robustness but less flexibility.

Cape Cod: Preferred when you have reliable prior information about ultimate severity levels. The separate row and column factors (19 parameters) provide flexibility but require more data to estimate reliably.

Berquist-Sherman: Use when you suspect systematic changes in development patterns over time. The explicit trend parameter (11 total) helps identify and quantify development year trends.

Hoerl Curve: Good for smooth development patterns. With only 5 model parameters, it’s parsimonious while still capturing key features. The mathematical form ensures sensible extrapolation.

Wright: Most flexible individual year treatment (13 parameters). Use when accident years have genuinely different characteristics that shouldn’t be constrained to a linear trend.

Model Uncertainty

As Hayne emphasizes, practitioners should “use multiple methods” because divergent forecasts indicate where underlying assumptions require investigation. The differences between models reflect model uncertainty - a key component of total reserve uncertainty often underappreciated in practice.

Conclusion

This tutorial demonstrated all five stochastic reserving models in

the stochasticreserver package:

- Chain Ladder: Simplest, most constrained

- Cape Cod: Exposure-based with separate factors

- Berquist-Sherman: Explicit development trend

- Hoerl: Smooth parametric curve

- Wright: Individual year levels

The unified maximum likelihood framework enables: 1. Consistent parameter estimation across models 2. Proper uncertainty quantification 3. Model comparison via information criteria 4. Monte Carlo simulation for reserve distributions

For production use, consider: - Running multiple models and comparing results - Examining residual diagnostics carefully - Using simulation to capture parameter uncertainty - Recognizing that model differences indicate structural uncertainty

References

Hayne, R. “A Flexible Framework for Stochastic Reserving Models.” Variance, Vol 7, Issue 2. Available at: https://variancejournal.org/article/120823

Session Information

## R version 4.5.2 (2025-10-31)

## Platform: x86_64-pc-linux-gnu

## Running under: Ubuntu 24.04.3 LTS

##

## Matrix products: default

## BLAS: /usr/lib/x86_64-linux-gnu/openblas-pthread/libblas.so.3

## LAPACK: /usr/lib/x86_64-linux-gnu/openblas-pthread/libopenblasp-r0.3.26.so; LAPACK version 3.12.0

##

## locale:

## [1] LC_CTYPE=C.UTF-8 LC_NUMERIC=C LC_TIME=C.UTF-8

## [4] LC_COLLATE=C.UTF-8 LC_MONETARY=C.UTF-8 LC_MESSAGES=C.UTF-8

## [7] LC_PAPER=C.UTF-8 LC_NAME=C LC_ADDRESS=C

## [10] LC_TELEPHONE=C LC_MEASUREMENT=C.UTF-8 LC_IDENTIFICATION=C

##

## time zone: UTC

## tzcode source: system (glibc)

##

## attached base packages:

## [1] stats graphics grDevices utils datasets methods base

##

## other attached packages:

## [1] abind_1.4-8 mvtnorm_1.3-3 stochasticreserver_0.1.1

##

## loaded via a namespace (and not attached):

## [1] digest_0.6.39 desc_1.4.3 R6_2.6.1 fastmap_1.2.0

## [5] xfun_0.56 cachem_1.1.0 knitr_1.51 htmltools_0.5.9

## [9] rmarkdown_2.30 lifecycle_1.0.5 cli_3.6.5 sass_0.4.10

## [13] pkgdown_2.2.0 textshaping_1.0.4 jquerylib_0.1.4 systemfonts_1.3.1

## [17] compiler_4.5.2 tools_4.5.2 ragg_1.5.0 evaluate_1.0.5

## [21] bslib_0.9.0 yaml_2.3.12 jsonlite_2.0.0 rlang_1.1.7

## [25] fs_1.6.6 MASS_7.3-65