Stochastic Reserving with RAA Data

2026-01-22

Introduction

This vignette demonstrates stochastic reserving methods using the RAA (Reinsurance Association of America) claims triangle from the ChainLadder package. This classic dataset contains general liability claims from 1981-1990 with 10 development periods.

The analysis parallels the original stochastic_reserving.Rmd vignette but uses publicly available data instead of the Hayne paper data.

Load Packages and Data

Initialize Triangle

The RAA data is cumulative paid claims in thousands of dollars. Unlike the Hayne paper data, we don’t have exposure counts, so we work directly with total claims rather than averages per exposure.

Show code

# Load RAA cumulative data from package

data(RAA_cumulative)

# Use RAA cumulative data as our development triangle

B0 <- RAA_cumulative

# Since RAA doesn't have exposure data, we use uniform exposure of 1

# This means we're modeling total claims rather than average claims

dnom <- rep(1, nrow(B0))

size <- nrow(B0)

# Display the data

cat("RAA Cumulative Claims Triangle (thousands USD)\n")RAA Cumulative Claims Triangle (thousands USD)Show code

print(B0) dev

origin 1 2 3 4 5 6 7 8 9 10

1981 5012 8269 10907 11805 13539 16181 18009 18608 18662 18834

1982 106 4285 5396 10666 13782 15599 15496 16169 16704 NA

1983 3410 8992 13873 16141 18735 22214 22863 23466 NA NA

1984 5655 11555 15766 21266 23425 26083 27067 NA NA NA

1985 1092 9565 15836 22169 25955 26180 NA NA NA NA

1986 1513 6445 11702 12935 15852 NA NA NA NA NA

1987 557 4020 10946 12314 NA NA NA NA NA NA

1988 1351 6947 13112 NA NA NA NA NA NA NA

1989 3133 5395 NA NA NA NA NA NA NA NA

1990 2063 NA NA NA NA NA NA NA NA NAModel Selection

Choose which reserving model to use. All five models from the Hayne framework are available:

- Berquist: Berquist-Sherman Incremental Severity

- CapeCod: Cape Cod method

- Hoerl: Generalized Hoerl Curve Model with trend

- Wright: Generalized Hoerl Curve with individual accident year levels

- Chain: Chain Ladder model

Show code

# Select model - try different models by changing this

model <- "Chain"

# model <- "Berquist"

# model <- "CapeCod"

# model <- "Hoerl"

# model <- "Wright"

# Toggle graphs and simulations

graphs <- TRUE

simulation <- TRUE

cat("Selected model:", model, "\n")Selected model: Chain Show code

cat("Model description:", model_description(model), "\n")Model description: Chain Ladder Model Calculate Incremental Matrix and Masks

Show code

Incremental Claims MatrixShow code

print(A0) 2 3 4 5 6 7 8 9 10

1981 5012 3257 2638 898 1734 2642 1828 599 54 172

1982 106 4179 1111 5270 3116 1817 -103 673 535 NA

1983 3410 5582 4881 2268 2594 3479 649 603 NA NA

1984 5655 5900 4211 5500 2159 2658 984 NA NA NA

1985 1092 8473 6271 6333 3786 225 NA NA NA NA

1986 1513 4932 5257 1233 2917 NA NA NA NA NA

1987 557 3463 6926 1368 NA NA NA NA NA NA

1988 1351 5596 6165 NA NA NA NA NA NA NA

1989 3133 2262 NA NA NA NA NA NA NA NA

1990 2063 NA NA NA NA NA NA NA NA NAShow code

# Generate a matrix to reflect exposure count in the variance structure

logd <- log(matrix(dnom, size, size))

# Set up matrix of rows and columns

rowNum <- row(A0)

colNum <- col(A0)

# Mask matrices

# upper_triangle_mask: allowable data (upper triangular)

# msn: first forecast diagonal

# msd: to-date diagonal

upper_triangle_mask <- (size - rowNum) >= colNum - 1

msn <- (size - rowNum) == colNum - 2

msd <- (size - rowNum) == colNum - 1

# Amount paid to date (cumulative to diagonal)

paid_to_date <- rowSums(B0 * msd, na.rm = TRUE)

cat("\nPaid to date by accident year:\n")

Paid to date by accident year:Show code

print(paid_to_date) 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990

18834 16704 23466 27067 26180 15852 12314 13112 5395 2063 Model-Specific Code

Show code

if (model == "Berquist") {

model_lst <- berquist(B0, paid_to_date, upper_triangle_mask)

} else if (model == "CapeCod") {

model_lst <- capecod(B0, paid_to_date, upper_triangle_mask)

} else if (model == "Hoerl") {

model_lst <- hoerl(B0, paid_to_date, upper_triangle_mask)

} else if (model == "Wright") {

model_lst <- wright(B0, paid_to_date, upper_triangle_mask)

} else if (model == "Chain") {

model_lst <- chain(B0, paid_to_date, upper_triangle_mask)

}

g_obj <- model_lst$g_obj

g_grad <- model_lst$g_grad

g_hess <- model_lst$g_hess

a0 <- model_lst$a0Negative Log-Likelihood Function

The objective function for maximum likelihood estimation. The model has parameters for both the loss model and the variance structure (power parameter and constant of proportionality).

Show code

l.obj <- function(a, A) {

npar <- length(a) - 2

e <- g_obj(a[1:npar])

v <- exp(-outer(logd[, 1], rep(a[npar + 1], size), "-")) * (e^2)^a[npar + 2]

t1 <- log(2 * pi * v) / 2

t2 <- (A - e)^2 / (2 * v)

sum(t1 + t2, na.rm = TRUE)

}

# Gradient of the objective function

l.grad <- function(a, A) {

npar <- length(a) - 2

p <- a[npar + 2]

Av <- aperm(array(A, c(size, size, npar)), c(3, 1, 2))

e <- g_obj(a[1:npar])

ev <- aperm(array(e, c(size, size, npar)), c(3, 1, 2))

v <- exp(-outer(logd[, 1], rep(a[npar + 1], size), "-")) * (e^2)^p

vv <- aperm(array(v, c(size, size, npar)), c(3, 1, 2))

dt <- rowSums(g_grad(a[1:npar]) * ((p / ev) + (ev - Av) / vv - p *

(Av - ev)^2 / (vv * ev)),

na.rm = TRUE,

dims = 1)

yy <- 1 - (A - e)^2 / v

dk <- sum(yy / 2, na.rm = TRUE)

dp <- sum(yy * log(e^2) / 2, na.rm = TRUE)

c(dt, dk, dp)

}Hessian of the Objective Function

-

eis the expected value matrix -

vis the matrix of variances -

A,e,vall have shapec(size, size)

Show code

l.hess <- function(a, A) {

npar <- length(a) - 2

p <- a[npar + 2]

Av <- aperm(array(A, c(size, size, npar)), c(3, 1, 2))

Am <- aperm(array(A, c(size, size, npar, npar)), c(3, 4, 1, 2))

e <- g_obj(a[1:npar])

ev <- aperm(array(e, c(size, size, npar)), c(3, 1, 2))

em <- aperm(array(e, c(size, size, npar, npar)), c(3, 4, 1, 2))

v <- exp(-outer(logd[, 1], rep(a[npar + 1], size), "-")) * (e^2)^p

vv <- aperm(array(v, c(size, size, npar)), c(3, 1, 2))

vm <- aperm(array(v, c(size, size, npar, npar)), c(3, 4, 1, 2))

g1 <- g_grad(a[1:npar])

gg <- aperm(array(g1, c(npar, size, size, npar)), c(4, 1, 2, 3))

gg <- gg * aperm(gg, c(2, 1, 3, 4))

gh <- g_hess(a[1:npar])

dtt <- rowSums(

gh * (p / em + (em - Am) / vm - p * (Am - em)^2 / (vm * em)) +

gg * (1 / vm + 4 * p * (Am - em) / (vm * em) +

p * (2 * p + 1) * (Am - em)^2 / (vm * em^2) - p / em^2),

dims = 2,

na.rm = TRUE

)

dkt <- rowSums((g1 * (Av - ev) + p * g1 * (Av - ev)^2 / ev) / vv,

na.rm = TRUE)

dtp <- rowSums(g1 * (1 / ev + (log(ev^2) * (Av - ev) +

(p * log(ev^2) - 1) * (Av - ev)^2 / ev) / vv),

na.rm = TRUE)

dkk <- sum((A - e)^2 / (2 * v), na.rm = TRUE)

dpk <- sum(log(e^2) * (A - e)^2 / (2 * v), na.rm = TRUE)

dpp <- sum(log(e^2)^2 * (A - e)^2 / (2 * v), na.rm = TRUE)

m1 <- rbind(array(dkt), c(dtp))

rbind(cbind(dtt, t(m1)), cbind(m1, rbind(cbind(dkk, c(dpk)), c(dpk, dpp))))

}Minimization

Starting Values

Use fitted objective function to get starting values for kappa and p parameters.

Actual Minimization

Model Statistics

Show code

Fitted Expected Values (mean): [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10]

[1,] 2458 3914 4010 2975 2087 1791 814 426 273 86

[2,] 2190 3487 3573 2651 1859 1596 726 380 243 77

[3,] 3122 4971 5093 3778 2650 2275 1034 541 346 109

[4,] 3687 5870 6013 4461 3129 2686 1221 639 409 129

[5,] 3734 5945 6091 4519 3170 2721 1237 647 414 131

[6,] 2523 4017 4116 3054 2142 1838 836 437 280 88

[7,] 2266 3608 3697 2743 1924 1651 751 393 251 79

[8,] 3105 4943 5064 3757 2635 2262 1028 538 344 109

[9,] 2081 3314 3395 2519 1767 1516 689 361 231 73

[10,] 2063 3285 3365 2497 1751 1503 683 358 229 72Show code

cat("\nParameter estimates:\n")

Parameter estimates:Variance power (p): 0.6629 Kappa: 3.9023 Information Matrix and Variance-Covariance

Show code

g1 <- g_grad(mle$par[1:npar])

gg <- aperm(array(g1, c(npar, size, size, npar)), c(4, 1, 2, 3))

gg <- gg * aperm(gg, c(2, 1, 3, 4))

meanv <- aperm(array(mean, c(size, size, npar)), c(3, 1, 2))

meanm <- aperm(array(mean, c(size, size, npar, npar)), c(3, 4, 1, 2))

varm <- aperm(array(var, c(size, size, npar, npar)), c(3, 4, 1, 2))

# Masks to screen out NA entries

s <- 0 * A0

sv <- aperm(array(s, c(size, size, npar)), c(3, 1, 2))

sm <- aperm(array(s, c(size, size, npar, npar)), c(3, 4, 1, 2))

# Second derivatives

tt <- rowSums(sm + gg * (1 / varm + 2 * p^2 / (meanm^2)), dims = 2, na.rm = TRUE)

kt <- p * rowSums(sv + g1 / meanv, na.rm = TRUE)

tp <- p * rowSums(sv + g1 * log(meanv^2) / meanv, na.rm = TRUE)

kk <- (1 / 2) * sum(1 + s, na.rm = TRUE)

pk <- (1 / 2) * sum(s + log(mean^2), na.rm = TRUE)

pp <- (1 / 2) * sum(s + log(mean^2)^2, na.rm = TRUE)

# Create information matrix

m1 <- rbind(array(kt), c(tp))

inf <- rbind(cbind(tt, t(m1)), cbind(m1, rbind(c(kk, pk), c(pk, pp))))

# Variance-covariance matrix

vcov <- solve(inf)Simulation

Run Monte Carlo simulation for distribution of future amounts.

Show code

sim <- matrix(0, 0, 11)

smn <- matrix(0, 0, 11)

spm <- matrix(0, 0, npar + 2)

nsim <- 5000

smsk <- aperm(array(c(upper_triangle_mask), c(size, size, nsim)), c(3, 1, 2))

smsn <- aperm(array(c(msn), c(size, size, nsim)), c(3, 1, 2))

if (simulation) {

for (i in 1:5) {

# Randomly generate parameters from multivariate normal

spar <- rmvnorm(nsim, mle$par, vcov)

# Arrays to calculate simulated means

esim <- g_obj(spar)

# Arrays to calculate simulated variances

ksim <- exp(aperm(outer(array(spar[, c(npar + 1)], c(nsim, size)),

log(dnom), "-"), c(1, 3, 2)))

psim <- array(spar[, npar + 2], c(nsim, size, size))

vsim <- ksim * (esim^2)^psim

# Randomly simulate future values

temp <- array(rnorm(nsim * size * size, c(esim), sqrt(c(vsim))),

c(nsim, size, size))

# Combine totals by exposure period and aggregate

sdnm <- t(matrix(dnom, size, nsim))

fore <- sdnm * rowSums(temp * !smsk, dims = 2)

forn <- sdnm * rowSums(temp * smsn, dims = 2)

# Cumulate results

sim <- rbind(sim, cbind(fore, rowSums(fore)))

smn <- rbind(smn, cbind(forn, rowSums(forn)))

spm <- rbind(spm, spar)

}

}Results

Reserve Estimates

Show code

cat("Model:", model, "\n")Model: Chain Show code

cat("Description:", model_description(model), "\n\n")Description: Chain Ladder Model Show code

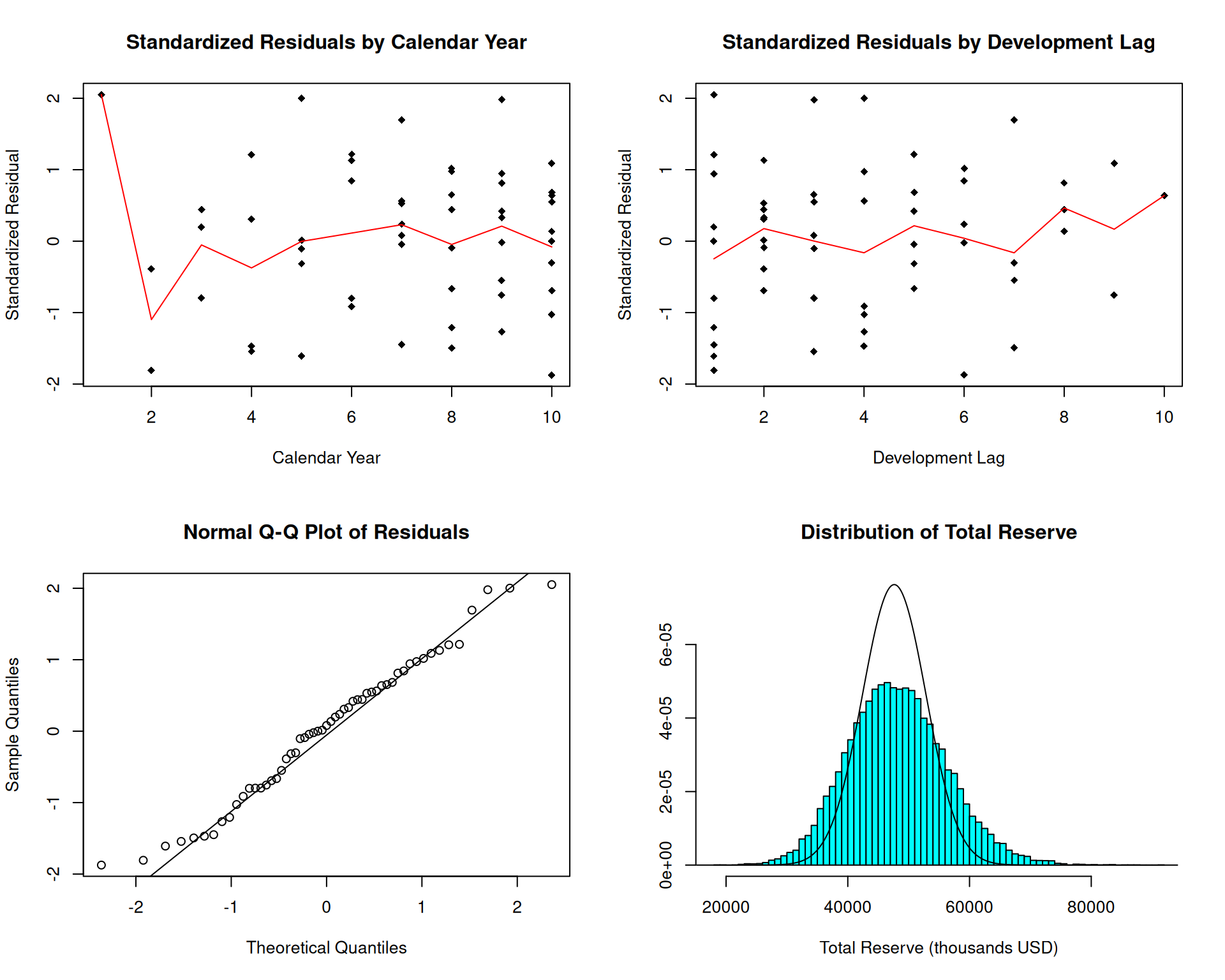

Point Estimate of Total Reserve: 47633 thousand USDShow code

Simulation Summary (Total Reserve):

Min. 1st Qu. Median Mean 3rd Qu. Max.

18067 42608 47868 48185 53385 91301 Diagnostic Plots

Show code

if (graphs) {

# Prep data for lines in scatter plots

ttt_plot <- array(cbind(c(rowNum + colNum - 1), c(stres)),

c(length(c(stres)), 2, 19))

sss_plot <- t(array(1:19, c(19, length(c(stres)))))

par(mfrow = c(2, 2))

# Residuals by Calendar Year

plot(

na.omit(cbind(c(rowNum + colNum - 1), c(stres))),

main = "Standardized Residuals by Calendar Year",

xlab = "Calendar Year",

ylab = "Standardized Residual",

pch = 18

)

lines(na.omit(list(

x = 1:19,

y = colSums(ttt_plot[, 2, ] * (ttt_plot[, 1, ] == sss_plot), na.rm = TRUE) /

colSums((ttt_plot[, 1, ] == sss_plot) + 0 * ttt_plot[, 2, ], na.rm = TRUE)

)), col = "red")

# Residuals by Lag

plot(

na.omit(cbind(c(colNum), c(stres))),

main = "Standardized Residuals by Development Lag",

xlab = "Development Lag",

ylab = "Standardized Residual",

pch = 18

)

lines(na.omit(list(

x = colNum[1, ],

y = colSums(stres, na.rm = TRUE) / colSums(1 + 0 * stres, na.rm = TRUE)

)), col = "red")

# Q-Q Plot

qqnorm(c(stres), main = "Normal Q-Q Plot of Residuals")

qqline(c(stres))

# Distribution of forecasts

if (simulation) {

proc <- list(

x = (density(sim[, 11]))$x,

y = dnorm((density(sim[, 11]))$x,

sum(matrix(c(dnom), size, size) * mean * !upper_triangle_mask),

sqrt(sum(matrix(c(dnom), size, size)^2 * var * !upper_triangle_mask)))

)

MASS::truehist(sim[, 11],

ymax = max(proc$y),

main = "Distribution of Total Reserve",

xlab = "Total Reserve (thousands USD)")

lines(proc)

}

}

Simulation Summary by Accident Year

Show code

if (simulation) {

sumr <- matrix(0, 0, 4)

sumn <- matrix(0, 0, 4)

for (i in 1:11) {

sumr <- rbind(sumr, c(mean(sim[, i]), sd(sim[, i]),

quantile(sim[, i], c(.05, .95))))

sumn <- rbind(sumn, c(mean(smn[, i]), sd(smn[, i]),

quantile(smn[, i], c(.05, .95))))

}

rownames(sumr) <- c(paste0("AY ", 1981:1990), "Total")

colnames(sumr) <- c("Mean", "Std Dev", "5%", "95%")

cat("\nReserve by Accident Year (thousands USD):\n")

print(round(sumr, 0))

rownames(sumn) <- c(paste0("AY ", 1981:1990), "Total")

colnames(sumn) <- c("Mean", "Std Dev", "5%", "95%")

cat("\nNext Period Forecast by Accident Year (thousands USD):\n")

print(round(sumn, 0))

}

Reserve by Accident Year (thousands USD):

Mean Std Dev 5% 95%

AY 1981 0 0 0 0

AY 1982 76 178 -185 374

AY 1983 452 488 -288 1282

AY 1984 1191 850 -148 2630

AY 1985 2434 1276 414 4591

AY 1986 3489 1506 1082 6029

AY 1987 5087 1827 2158 8175

AY 1988 10744 3048 5939 15883

AY 1989 10651 2958 5987 15678

AY 1990 14061 3908 8205 20906

Total 48185 8051 35633 61933

Next Period Forecast by Accident Year (thousands USD):

Mean Std Dev 5% 95%

AY 1981 0 0 0 0

AY 1982 76 178 -185 374

AY 1983 343 420 -265 1084

AY 1984 649 606 -243 1710

AY 1985 1244 903 -140 2805

AY 1986 1839 1134 57 3800

AY 1987 1939 1156 100 3919

AY 1988 3772 1825 892 6912

AY 1989 3418 1689 739 6275

AY 1990 3365 1715 705 6268

Total 16646 3627 10851 22726Data Attribution

The RAA data used in this vignette is from the Reinsurance Association of America, obtained via the ChainLadder R package.

Citation: Gesmann M, Murphy D, Zhang Y, Carrato A, Wuthrich M, Concina F, Dal Moro E (2025). ChainLadder: Statistical Methods and Models for Claims Reserving in General Insurance. R package version 0.2.20. https://mages.github.io/ChainLadder/